“China is a sleeping giant. Let her sleep, for when she wakes, she will shake the world.” -Napoleon Bonaparte

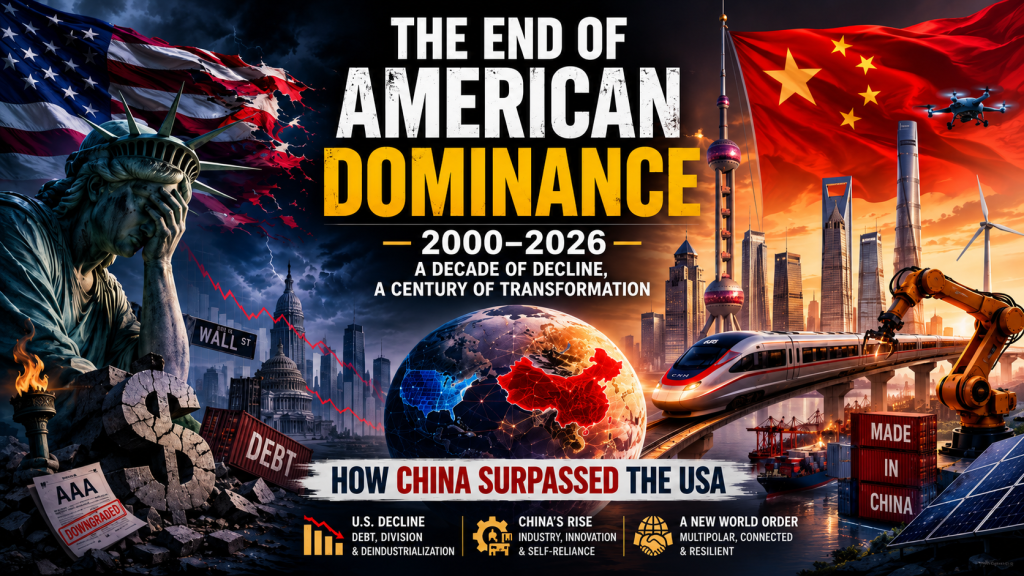

The decade between 2000 to 2026 will be recorded in history as the period when the world’s unipolar moment dominated entirely by American financial, military, and cultural power quietly but decisively ended. This was not a single dramatic rupture. It was a slow accumulation of structural rot on one side and methodical strategic construction on the other.

On one side: the United States, distracted by internal culture wars, addicted to financial speculation, and paralysed by a polarisation so severe that its own institutions have started to visibly malfunction. On the other: China, executing a decades-long industrial policy with the precision of a state that does not ask voters for permission between five-year plans.

The numbers tell the story coldly. Adjusted for Purchasing Power Parity (PPP), the measure economists use to compare what money actually buys in real economies. China’s GDP is already approximately 20 percent larger than that of the United States. Its manufacturing capacity is twice that of any competitor. By 2030, it is projected to account for 35 percent of all global manufacturing output. The US will account for 11 percent. This is not a rivalry. This is a transition.

Trump accepts USA decline as a superpower

For much of its modern history, the United States operated from a position of absolute primacy. it set the rules, it enforced them, and it rarely needed to negotiate as an equal. That posture has collapsed. What we are witnessing today from Washington is not confident global leadership. It is the rhetoric of managed retreat.

The “America First” doctrine, in both its 2017 and 2025 incarnations, was sold as aggressive nationalism. In reality, it was a tacit acknowledgement that America could no longer afford the cost of its own empire. Trade deals were renegotiated not to expand American dominance but to limit its losses. Bilateral trade “boards” with China. The kind of pragmatic, face-saving summitry that Washington would have rejected as beneath it in 1995 became the new diplomatic reality. These are not the actions of a hegemonic power; they are the actions of a debtor nation negotiating with its banker.

Trump’s own statements have, at moments, stripped away the pretence. His repeated framing of America as a nation being “ripped off,” “taken advantage of,” and “destroyed from within” is whatever the political intent a presidential acknowledgement that the old order is broken. The US has moved from dictating terms to seeking arrangements. That is a historic pivot. And Beijing noticed it years before Washington admitted it.

In May 2025, Moody’s downgraded the US credit rating from AAA to Aa1, the first downgrade since 1917. This was not a partisan verdict. It was a financial institution acknowledging what economists had been warning about for years: the structural unsustainability of American fiscal policy.

Key reasons for USA’s decline as a superpower

America’s decline is not a conspiracy. It is an accounting problem. one that accumulated across decades of deliberate policy choices, and is now too large to paper over.

The Fiscal Trap

As of Q4 2025, the US debt-to-GDP ratio stands at 122.3%, with total national debt exceeding $38.5 trillion. Annual interest payments on this debt have crossed $1 trillion exceeding the entire US defence budget. The country is now, in a very literal sense, spending more to service past decisions than to prepare for the future. Research consistently shows that debt-to-GDP ratios above 77% begin to suppress long-term economic growth. America is nearly 50 percentage points past that threshold.

The Hollowed-Out Economy

Over the past four decades, the United States systematically dismantled its manufacturing base in favour of financialisation the model of generating wealth through financial instruments rather than producing goods. This created extraordinary returns for the top percentile and gutted the industrial middle class. By 2026, the US accounts for just 11 percent of global manufacturing output. It runs on consumption and debt, importing the goods its citizens need from the very country it competes with geopolitically.

Political and Social Fracture

Freedom House’s 2026 report ranks the United States at a score of 81. its lowest on record, tied with South Africa, and below Panama. Over two decades, the US score has dropped 12 points. The country that once exported democracy as an aspirational brand now struggles to demonstrate its own institutional stability. Legislative gridlock has made long-term economic planning virtually impossible. Military adventures in Iraq, Afghanistan, Libya, and the 2026 Iran war have drained trillions of dollars from domestic investment. The cumulative cost of post-9/11 conflicts alone exceeds $8 trillion by most estimates resources that could have rebuilt American infrastructure, funded universal broadband, or re-industrialised the rust belt.

How China became self-sufficient and beat the USA without dollar hegemony

China’s rise is not accidental. It is the product of a patient, multi-decade industrial strategy executed with a consistency that democratic systems where policy resets every four years structurally cannot match.

The Manufacturing Asymmetry

China produces over two-thirds of the world’s electric vehicles, more than 75 percent of global battery output, and 80 percent of all solar panels. BYD. once dismissed by Elon Musk has surpassed Tesla in market value and now outranks Ford, GM, and Volkswagen. This is not just market share; it is structural leverage. China controls the hardware of the energy transition. Every country building a green economy must, at some point, pass through Beijing’s supply chain.

Bypassing the Dollar

For decades, the United States weaponised dollar hegemony the fact that global trade, oil markets, and sovereign reserves are denominated in USD as a geopolitical tool. Sanctions, financial exclusions, and SWIFT cutoffs became instruments of foreign policy. China studied this, understood the vulnerability it created, and systematically built an exit architecture.

The BRICS+ bloc, now encompassing countries that collectively represent a substantial portion of global GDP and population, has accelerated local currency settlement frameworks. The mBridge system a blockchain-based cross-border payment infrastructure connecting China, Hong Kong, Thailand, the UAE, and Saudi Arabia is operational and scaling. Foreign governments issued a record 13 billion yuan in Panda bonds in 2025, signalling growing appetite for yuan-denominated finance. The Belt and Road Initiative (BRI), whatever its implementation flaws, has anchored over 140 countries into infrastructure relationships with China relationships that generate loyalty, trade flows, and long-term yuan adoption outside the SWIFT architecture.

Critical distinction: In nominal USD terms, the US economy remains larger. But nominal GDP reflects currency strength and financial complexity not real productive capacity. In PPP terms, which measures actual goods and services produced, China is already ahead. The US lead exists on paper. China’s lead exists in factories, ports, and battery gigaplants.

Why India has lesser development in comparison to China

Comparisons between India and China are politically sensitive but analytically necessary. Both are ancient civilisations with vast populations and legitimate superpower ambitions. But on the question of developmental trajectory over the last three decades, the data is unsparing.

India’s nominal GDP in 2025 stands at approximately $4.1 trillion. China’s is over $18 trillion. In PPP terms the gap narrows to roughly 2.5:1 but even that framing understates the structural divergence.

The Infrastructure Execution Gap

China’s highway network is five times larger than India’s. China built its high-speed rail empire the largest in the world in roughly 15 years through state-directed investment and expedited land acquisition. India’s infrastructure projects routinely stall for years over land acquisition disputes, environmental clearances, and inter-ministerial coordination failures. Democratic accountability, while a fundamental value, creates friction that authoritarian planning systems do not experience. China chose speed. India inherited complexity.

The Manufacturing vs. Services Trap

India’s most celebrated economic achievement its IT and services sector is also its structural constraint. Services employ highly educated urban workers but cannot absorb the hundreds of millions of semi-skilled and unskilled workers that India’s demographic dividend represents. India needs to create more than 10 million formal-sector jobs annually simply to keep pace with its workforce growth. Manufacturing, which does that work, accounts for less than 20 percent of India’s GDP compared to China’s roughly 28 percent at a comparable stage. India skipped industrialisation and went from agriculture to services, bypassing the mass-employment manufacturing phase that created China’s middle class.

Automation and Productivity

India’s factory automation rate stands below 30 percent. China’s exceeds 50 percent. This is not merely a technology gap it is a productivity multiplier gap. Indian manufacturing can compete on labour cost at the low end of the value chain, but as products increase in complexity, the absence of integrated automation, logistics infrastructure, and supplier ecosystems becomes a ceiling, not just a constraint. China’s “Made in China 2025” strategy anticipated this and invested accordingly in robotics, AI-integrated production, and precision manufacturing. India’s equivalent initiatives are real but a decade behind in execution.

The Structural Potential

None of this is permanent. India holds advantages that China does not: a median worker age of 28 compared to China’s 39, a growing consumer market projected to reach $4.3 trillion by 2030, and a democratic political system that generates long-run institutional trust from foreign investors. The question is not whether India will grow. It will. The question is whether it will grow fast enough, and in manufacturing depth, to reshape the global order rather than benefit from it on the margins.

USA credibility continues to fall

Hard power military capacity, economic size can be measured. Soft power is harder to quantify and much harder to rebuild once lost. The United States is experiencing a soft power haemorrhage that no defence budget can stop.

The Weaponisation of the Dollar

When the US seized Russian sovereign reserves following the 2022 Ukraine invasion, it sent an unmistakable signal to every country in the world that holds dollar-denominated assets: your savings are secure only as long as Washington approves of your government. This single act accelerated de-dollarisation faster than any Chinese propaganda campaign could have. Nations that had no particular alignment with Russia or China began diversifying their reserves and trade settlement arrangements — not out of ideology, but out of elementary financial risk management.

The Reliability Problem

For the Global South, the fundamental problem with American partnership is unpredictability. The Obama administration committed to the Paris Agreement. Trump withdrew. Biden re-joined. Trump withdrew again. The JCPOA with Iran was signed, abandoned, partially revived, then bombed into irrelevance in 2026. Trans-Pacific Partnership, abandoned. NATO commitments, intermittently questioned. A country cannot lead a rules-based international order if it treats rules as optional depending on who won the last election. China’s BRI projects, whatever their debt terms, arrive with a consistent counterparty. Washington’s development promises arrive with an expiration date tied to the electoral calendar.

The Vacuum Beijing is Filling

While Washington debated its own legitimacy, Beijing was building ports in Sri Lanka, railways in Kenya, power plants in Pakistan, and digital infrastructure across Southeast Asia. Whether one views these projects with suspicion or appreciation is secondary to their impact: nations that once looked to Washington for development partnership are now looking east. The multipolar world is not a future scenario. It is the present reality. The contest now is not whether multipolarity exists, but who will write its rules.

The century belongs to those who build

The 21st century will not be “owned” by any single nation in the way the 20th was owned by America. But if the last decade has taught the world anything, it is this: the nations that build infrastructure, manufacture goods, control supply chains, and offer consistent partnership to the developing world will set the agenda. The nations that financialise their economies, export their manufacturing, wage expensive wars, and confuse Twitter diplomacy for statecraft will not.

China has not won the future. But for the first time in a century, America is no longer the default answer to who will.