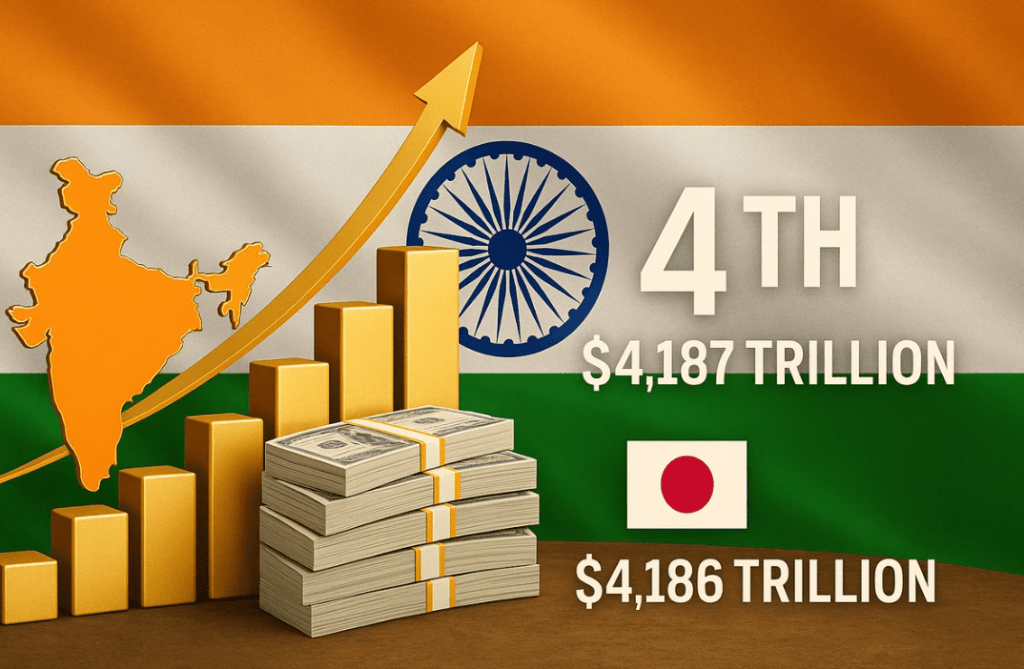

India has emerged as the world’s fourth-largest economy, overtaking Japan with a gross domestic product (GDP) valued at $4.18 trillion, according to the Indian government’s end-of-year economic review. The milestone marks another major step in India’s rapid economic ascent and places it behind only the United States, China, and Germany.

The government’s assessment, released late Monday, said India is among the fastest-growing major economies globally and is well-positioned to sustain its growth momentum despite ongoing global trade uncertainties. While official confirmation of the ranking will depend on final annual GDP figures due in 2026, projections from the International Monetary Fund (IMF) support the claim. The IMF estimates India’s GDP will reach $4.51 trillion in 2026, slightly ahead of Japan’s projected $4.46 trillion.

India’s economic rise comes at a time of heightened global volatility. In August, Washington imposed significant tariffs on Indian goods over New Delhi’s continued purchases of Russian oil, raising concerns about trade disruptions. Despite this, the government said India’s growth reflects its economic resilience amid persistent global headwinds.

Officials are optimistic that India could overtake Germany to become the world’s third-largest economy within the next two-and-a-half to three years, with GDP projected to reach $7.3 trillion by 2030. India had already surpassed Britain in 2022 to become the world’s fifth-largest economy.

However, the strong headline GDP numbers mask underlying challenges. India’s GDP per capita remains low, standing at $2,694 in 2024, according to World Bank data, significantly lower than Japan’s $32,487 and Germany’s $56,103. This highlights the gap between aggregate economic size and individual living standards.

Employment remains another major concern. More than a quarter of India’s 1.4 billion population is aged between 10 and 26, creating immense pressure on the labour market. The government acknowledged the need to generate quality, well-paying jobs to productively absorb the expanding workforce and ensure inclusive growth.

In response to slowing growth earlier this year, Prime Minister Narendra Modi introduced sweeping consumption tax cuts and advanced labour law reforms. Nevertheless, economic pressures persist. The Indian rupee hit a record low against the US dollar in December, falling around five percent in 2025 amid trade uncertainties and export concerns.

While 2025 offers much to celebrate for India’s economy, experts note that sustaining long-term growth will depend on strengthening exports, stabilising the currency, and ensuring that economic expansion translates into improved livelihoods for its vast population.